- The Capital Challenge

- Posts

- A Psychological Analysis of your Money

A Psychological Analysis of your Money

Putting a perspective on how we view finance

Justin Schlendorf

August 26, 2024

Your personal experiences with money make up maybe 0.000001% of what has happened in the world, but maybe 80% of how you think the world works.

The Money Perspective:

The environment you grew up in vastly determines the outlook you have on finances.

Take for example a study conducted in 2006:

Economists Ulrike Malmendier and Stefan Nagel dug through 50 years of the Survey of Consumer Finances and found this:

The way you view money is dependent on the environment you were born into:

If you grew up when inflation was high, you invested less money in bonds later in life compared to those who grew up when inflation was low

If you happened to grow up when the stock market was strong, you invested more of your money in stocks later in life compared to those who grew up when stocks were weak.

This underlines that you should separate your current financial knowledge from the new one you will acquire.

Your family, generation, and lifestyle all determine your financial outlook.

The Average American:

Americans spend more money on lottery tickets than, drum roll, please……

Movies

Video games

Music

Sporting events

Books

All Combined!

I share this to give perspective on why so many people are poor, so let’s look.

“ The lowest income households in the U.S. average spend $412 a year on lottery tickets, 4x the amount of those in the highest income groups.

40% of Americans cannot come up with $400 in an emergency. “

- Psychology of Money by Morgan Housel

Americans are spending their emergency fund on lottery tickets!

The Poor Persons Perspective:

Let us take a look from their perspective as to why this behavior might occur.

For their argument's sake, someone in their position might say:

“ We live paycheck to paycheck and saving seems out of reach, our hope for higher wages seems out of reach.

Buying a lottery ticket is the only time we can hold a tangible dream of getting the good stuff the wealthy take for granted.

We pay for a dream, so we buy more than you do. “

How do we set ourselves up for financial success?

A Psychological Framework for Financial Success:

Compounding:

Compounding doesn’t rely on earning big returns.

Merely good returns that are sustained uninterrupted for the longest period; especially in times of chaos and havoc.

The idea is the longer you have your money invested the higher the exponential growth for your money.

The cost: Time

$81.5 billion of Warren Buffet’s $84.5 billion net worth came after his 65th birthday.

A method we can use to maximize our compounding efforts uses the stock market as a vehicle for financial success.

Dollar Cost Averaging:

Investing a fixed amount into an investment over a long period regardless of the price

This chart demonstrates the power dynamics in dollar cost averaging as a compounding method.

In my current situation, I am investing $50 a week into index funds. My portfolio comprises companies based in AI, technology, and gold.

I am putting most of my funds into tech companies as I foresee a massive return on my money 20-40 years later.

I am Dollar Cost Averaging every week no matter the price of these indexes, here is my current portfolio as of this writing:

I am currently 3 months into consistent investing for perspective.

Consider what would happen if you invested $1 every month from 1900 - 2019:

You could invest that $1 into the U.S. stock market every month, rain or shine.

No matter if economists are screaming about a looming recession or a new bear market you just kept investing - Let’s call that investor Sue.

But maybe investing during a recession is too scary; so perhaps you invest your $1 in the stock market when the economy is not in a recession.

Sell everything when it is in a recession and save your monthly dollars in cash, then invest when the recession is over again. - Let’s call that investor Jim.

Or Perhaps it takes a few months for a recession to scare you out, and then it takes a while to regain confidence before you get back in the market.

You invest in stocks when there’s no recession, sell six months after a recession begins, and invest back six months after the recession ends. - Let’s call you Tom.

How much money would these 3 investors end up with over time?

Sue: $435,551

Jim: $257,386

Tom: $234,476

Sue is the clear winner.

During the time 300 months out of 1400 were a recession. By her continual investments through these recessions, she ends up with almost 3 quarters more money than Jim and Tom.

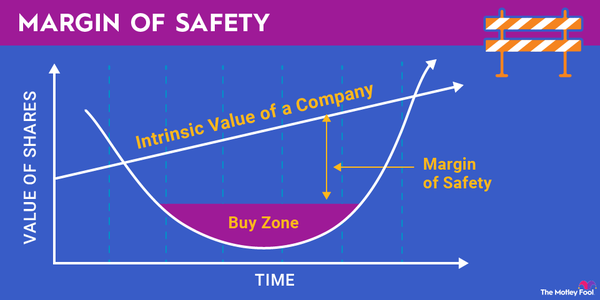

The Margin of Safety:

the room for error in a risk-taking activity

This can apply to your finances, investments, sales for a business, and any risk-taking you do.

The Margin of Safety is the psychology that if your investments only return 5% when they were supposed to return 10%, you are OK.

Start structuring your investments like this:

Fixed Investment: $$ per (time frame: day, week, month)

Projected Returns: %

The Margin of Safety: %

This structure allows you to feel comfortable when your money isn’t returning what you expected.

Get used to everything you thought not happening at all.

The biggest way to overcome this fear is by having that margin of safety that acts like a safety net.

Why are you not saving more?

Savings can be created by spending less. You can spend less if you desire less. And you will desire less if you care less about what others think of you.

You might think you want an expensive car, a fancy watch, and a huge house; but what you want is respect and admiration from other people.

Having expensive stuff never brings that from people, especially the ones you want to respect you.

Building wealth has little to do with your income or investment returns and lots to do with your savings rate.

You can build wealth without a high income, but can’t without a high savings rate.

For example:

John earns $50,000 a year. He saves 10% for the year.

Johns savings: $5,000

Mark earns $500,000 a year. He doesn’t save because he makes “enough money”.

Mark filed for bankruptcy 5 years later because he was fired and couldn't give up his $500,000 lifestyle, Mark lived paycheck to paycheck.

John now has $25,000 which he puts down on his first rental property.

John will take longer to build financial freedom but is well on track because he saves.

Mark chooses not to because of his temporary situation until it doesn’t work out anymore.

This example is exaggerated for effect, but is meant to deliver the point of saving!

Save for no reason:

Get in the habit of saving to save.

Wealth is the income not spent. It has the option not yet taken to buy something later.

Saving without a spending goal provides options and flexibility.

Wealth Builder:

The biggest single point of failure with money is a sole reliance on a paycheck to fund short-term spending needs.

Create a gap between what you think your expenses are and what they might be in the future.

Saving money is the gap between your ego and your income, and wealth is what you don’t see

Wealth is created by depressing what you could buy today to have more options in the future

Manage your money in a way that helps you sleep at night

Money should be a tool you use to gain control over your time.

The ability to do what you want, how you want, with who you want is the highest dividend money can pay

Additional Resources:

Reply